Data Management in Tally

How are Imports and Exports Treated in GST

Taxation laws have laid down the taxes applicable on import and export of goods and services. In the current tax regime, laws of Customs duty, Excise, Service Tax and VAT lay down the tax treatment of imports and exports. In the GST regime, Excise, Service Tax and VAT will be subsumed into GST and customs duty will continue to be levied separately. Let us understand the tax implication on imports and exports under GST in comparison to the current regime.

Current Regime

Import of goods

In the current regime, a person who imports goods has to pay customs duty, countervailing duty (CVD), and special additional duty (SAD). CVD is levied at a rate equivalent to the rate of Excise on such goods, if they had been manufactured in India. SAD is equivalent to VAT on the goods in India. CVD and SAD are imposed to bring the imported product’s price to its true market price in India. If the importer uses the imported goods to manufacture dutiable goods in India or provide taxable services, CVD paid on inputs is available as tax credit. If the importer is just a trader, CVD on imports is not available as credit. SAD paid on import is eligible for refund, subject to conditions. However, no credit is given on customs duty paid and it becomes a cost for the importer.

Let us see an example to understand the levy of import duties in case of import of goods in the current regime.

Example: Manoj Apparel in Bangalore, Karnataka purchases apparel from a supplier, Oz Designs, in Sydney, Australia.

Tax calculation

| Particulars | Nos. | Price per no. (Rs.) | Amount(Rs.) |

|---|---|---|---|

| Women’s T-shirts | 200 | 2,500 (51.68 AUD) * | 5,00,000 |

| Men’s T-shirts | 100 | 5,000 (103.37 AUD) * | 5,00,000 |

| Total | 300 | – | 10,00,000 |

| Customs duty @ 10% | Â | Â | Â 1,00,000 |

| Customs education cess @ 3% on customs duty (1,00,000*3%) | Â | Â | Â Â Â Â 3,000 |

| Sub total | Â | Â | 11, 03,000 |

| CVD @ 12.5% | Â | Â | Â 1,37,875 |

| Sub total | Â | Â | 12,40,875 |

| SAD @ 4% | Â | Â | Â Â Â 49,635 |

| Total cost of import | Â | Â | 12,90,510 |

* Exchange rate taken is 0.021 AUD = 1 Rupee

Import of services

A person who imports services has to pay Service Tax on the imported service at the Service tax rate applicable in India. The importer can claim tax credit of the Service Tax paid on imports.

For example: Rajesh Apparels in Hyderabad, Telengana, avails fashion designing services of Rs. 50,00,000 from Kaushi Designs in Colombo, Sri Lanka.

Tax calculation

| Particulars | Amount (Rs.) |

|---|---|

| Fashion designing services | Â 50,00,000 |

| Service Tax @14% | Â Â Â 7,00,000 |

| Krishi Kalyan Cess @0.5% | Â Â Â Â Â Â 25,000 |

| Swachh Bharat Cess @0.5% | Â Â Â Â Â Â 25,000 |

| Total cost of import | Â 57,50,000 |

Exports

In the current regime, export of goods and services is zero rated, i.e. rate of tax on exports is 0%. An exporter can also claim refund of the tax paid on inputs used to manufacture/purchase/provide the exported goods or services.

GST Regime

Import of goods

In the GST regime, a person who imports goods has to pay customs duty and IGST. The difference here is that CVD and SAD levied on imports in the current regime will be replaced by IGST under GST. IGST will be levied at the rate applicable to the imported goods in India. An importer can claim full tax credit of IGST paid on imports. Hence, importers who were unable to claim credit of CVD or SAD in the current regime can now claim full tax credit of the IGST paid on imports. However, no tax credit will be given on customs duty paid and it remains a cost for the importer under GST also.

Let us take an example to understand the levy of import duties in case of import of goods in the GST regime.

Example: Manoj Apparel in Bangalore, Karnataka purchases apparel from a supplier, Oz Designs, in Sydney, Australia.

Tax calculation

| Particulars | Nos. | Price per no. (Rs.) | Total Price (Rs.) |

|---|---|---|---|

| Women’s T-shirts | 200 | 2,500    (51.68 AUD) * |  5,00,000 |

| Men’s T-shirts | 100 | 5,000    (103.37 AUD) * |  5,00,000 |

| Total | 300 | – | 10,00,000 |

| Customs duty @ 10% | Â | Â | Â Â 1,00,000 |

| Education cess @ 3% on customs duty (10,000*3%) | Â | Â | Â Â Â Â Â 3,000 |

| Sub total | Â | Â | 11,03,000 |

| IGST @18% ** | Â | Â | Â 1,98,540 |

| Total cost of import | Â | Â | 13,01,540 |

* Exchange rate taken is 0.021 AUD = 1 Rupee

**Assuming GST rate of 18% on apparel.

Import of Services

Under GST, a supply will be considered as an import of service when-

- The supplier of the service is located outside India.

- The recipient of the service is located in India and

- The place of supply of the service is in India.

For example: Rajesh Apparels in Hyderabad, Telengana, avails fashion designing services of INR 50,00,000 from Kaushi Designs in Colombo, Sri Lanka

Location of supplier: Colombo, Sri Lanka

Location of recipient: Hyderabad, Telengana

Place of supply: Place of supply will be the location of the recipient, i.e. Hyderabad, Telengana.

Hence, this supply is an import.

Tax calculation

| Particulars | Amount (Rs.) |

|---|---|

| Fashion designing services | Â 50,00,000 |

| IGST @ 18%* | Â Â Â 9,00,000 |

| Total cost of import | Â 59,00,000 |

* Assuming GST rate of 18% on fashion designing services

Exports

Under GST, exports will be zero rated, similar to the current regime. An exporter can also claim refund of the tax paid on inputs used to manufacture/purchase/provide the exported goods or services.

Export of services

Specific conditions have been laid down for a supply to be considered an export of service under GST. These are:

- The supplier of the service is located in India.

- The recipient of the service is located outside India.

- The place of supply of the service is outside India

- The payment for the service has been received by the supplier in convertible foreign exchange and

- The supplier and recipient are not establishments of the same person.

For example: Rohan Consultants in Mumbai, Maharashtra, provides business consultancy services to Abey’s Engineering in Singapore. The payment for the service has been received in Singapore Dollars.

Here,

Location of supplier: Mumbai, Maharashtra

Location of recipient: Singapore

Place of supply: Place of supply will be the location of the recipient, i.e. Singapore.

Payment for the service:Â Payment for the service has been received in convertible foreign exchange, i.e. Singapore Dollars.

Relationship between the supplier and recipient:Â The supplier and recipient are distinct persons.

Hence, this supply qualifies as an export of service. Rate of tax on the supply will be 0%.

The levy of taxes and treatment of taxes in case of imports and exports largely remain the same under GST in comparison with the existing laws. In case of an importer, full input credit will be available on the IGST paid on imports and additional input credit will be available on the GST paid on all types of inputs used or intended to be used in the course of or for the furtherance of business. Similarly, in the case of an exporter, refund will be given on the tax paid on all inputs used in the course of business. Overall, costs of import and export are expected to reduce under GST and compliance is expected to become easier with the convergence of multiple tax laws into one law.

What are the Accounts and other Records you should Maintain under GST

Accounts and records are the primary source of data for any organization’s financial reporting. Every law of Direct and Indirect Tax in our country also mandates that information in a prescribed manner has to be captured and preserved for a certain period of time. These accounts and records form the basis for returns filed by tax payers under each law.

Current regime

In the current indirect tax regime, every tax law mandates certain accounts and records of transactions to be maintained for a specific period of time, apart from the regular books of accounts.

Under Excise, the general records to be maintained are the RG-1 register (Daily stock account of excisable goods), Form IV register (Register of receipt or issue of raw material), invoice book and job work register

Under Service Tax, the suggested records include the bill register, receipt register, debit/credit notes register, CENVAT credit register, etc

Under VAT, the records to be maintained include purchase records, sales records, stock records, VAT account containing details of input and output tax, works contract account, etc

These records are required to be retained for at least 5 years from the end of the financial year in which they were effected.

GST regime

Under GST, the activities of manufacture, provision of taxable service and sale of goods will have a common law and hence, businesses can now maintain consolidated information which was maintained separately earlier.

Under GST, every registered taxable person is required to maintain correct accounts of the following details at the principal place of business specified in the registration certificate: –

- Manufacture of goods

- Inward and outward supply of goods and/or services

- Stock of goods

- Input tax credit availed

- Output tax payable and paid

If more than one place of business is specified in the registration certificate, accounts relating to each place of business must be kept at the respective places.

Maintaining books and records in electronic form will be ideal and convenient for accurate and timely compliance under GST.

Persons whose turnover during the financial year exceeds Rs. 1 crore

In addition to maintaining the accounts specified above, a registered person whose turnover during the financial year exceeds Rs. 1 crore is required to,

- Get the accounts audited by a Chartered Accountant or Cost Accountant and

- Submit a copy of the audited annual accounts and a reconciliation statement in Form GSTR- 9B while filing the annual return in Form GSTR-9.

In the reconciliation statement, the Chartered Accountant or Cost Accountant is required to certify that the value of supplies declared in the annual return reconciles with the audited annual financial statement.

Persons owning or operating a warehouse or godown

An owner or operator of a warehouse or godown or any other place used for storage of goods, irrespective of whether he is registered or not, is required to maintain records of the consignor, consignee and other details which are yet to be prescribed in the law.

How long should accounts and records be retained?

Every registered person is required to retain accounts and records for 5 years from the due date of filing of annual return for the year to which the accounts and records pertain.

For example: For accounts and records pertaining to Financial Year ’17-’18, annual return must be filed by 31st December ’18. These accounts and records must be retained till 31st December ’23.

Invoicing under GST

Invoicing is a crucial aspect of tax compliance for every business. It is essential to be aware of the rules of invoicing under GST. Let us understand these in detail.

Invoicing in the current tax regimes

In the current tax regimes, tw

o types of invoices are issued:

- Tax invoice – This is issued to registered dealers, and can be used to claim tax credit. Sample formats of the two main types of tax invoice in the current tax regime, the Rule 11 Excise invoice and tax invoice are shown below.

- Retail or commercial invoice – This is issued to an unregistered dealer or retail customer, and no tax credit can be claimed on this invoice. Sample format of a retail invoice in the current tax regime is shown below.

Invoicing in the GST regime

In the GST regime, two types of invoices will be issued:

- Tax invoice

- Bill of supply

Tax invoice

When a registered taxable person supplies taxable goods or services, a tax invoice is issued. Based on the rules regarding details required in a tax invoice, a sample tax invoice has been shown below.

What is the time limit for issue of tax invoice?

| Supply of goods | The tax invoice must be issued before or at the time ofRemoval of goods, where supply involves movement of goods

E.g. – When Super Cars Ltd, a car manufacturer, supplies cars to its dealer Ravindra Automobiles, the invoice must be issued at the time of removal of the cars from Super Cars Ltd’s premises. This is because the supply involves movement of the cars to Ravindra Automobiles’ premises. OR Delivery of goods to the recipient, where supply does not require movement of goods E.g. – Super Cars Ltd purchases a generator set, which will be assembled and installed at the factory premises by the supplier. Here, since the supply does not require movement of the generator set, the invoice must be issued at the time when the generator set is made available to Super Cars Ltd. |

| Supply of services | The tax invoice must be issued within 30 days from the date of supply of the service. Where the supplier is a bank or any financial institution, the invoice must be issued within 45 days of the supply of service. |

Note: In case a person paying tax on reverse charge receives goods or services from an unregistered supplier, the receiver must issue an invoice on the date of receipt of goods or services.

How many copies of the tax invoice are required?

For supply of goods, three copies of the invoice are required – Original, Duplicate, and Triplicate.

Original invoice: The original invoice is issued to the receiver, and is marked as ‘Original for recipient’.

Duplicate copy: The duplicate copy is issued to the transporter, and is marked as ‘Duplicate for transporter’. This is not required if the supplier has obtained an invoice reference number. The Invoice reference number is given to a supplier when he uploads a tax invoice issued by him in the GST portal. It is valid for 30 days from the date of upload of invoice.

Triplicate copy: This copy is retained by the supplier, and is marked as ‘Triplicate for supplier’.

For supply of services, two copies of the invoice are required:

- Original Invoice: The original copy of the invoice is to be given to receiver, and is marked as ‘Original for recipient’.

- Duplicate Copy: The duplicate copy is for the supplier, and is marked as ‘Duplicate for supplier’.

What details must a tax invoice for export contain?

An export invoice must, in addition to the details required in a tax invoice, contain the following details:

| Export invoice |

|---|

| Must have the words ‘“Supply meant for export on payment of IGST†or “Supply meant for export under bond without payment of IGST†|

| Name and address of the recipient |

| Delivery address |

| Number and date of ARE-1 (application for removal of goods for export) |

Bill of Supply

Bill of Supply is to be issued by a registered supplier in the following cases:

- Supply of exempted goods or services

- Supplier is paying tax under composition scheme

Based on the rules regarding details required in a Bill of supply, a sample Bill of Supply has been shown below.

The bill of supply need not be issued when the value of goods or services supplied is less than Rs 100, unless the receiver insists for the bill. However, a consolidated bill of supply should be prepared at the end of the business day for all such supplies for which the bill of supply is not issued.

How to revise the values of an invoice already issued?

To revise the taxable value or GST charged in an invoice, a debit note or supplementary invoice or credit note must be issued by the supplier.

Debit note/supplementary invoice- These are to be issued by a supplier to record increase in taxable value &/or GST charged in the original invoice.

Credit note- These are to be issued by a supplier to record decrease in taxable value &/or GST charged in the original invoice. Credit note must be issued on or before 30th September following the end of the financial year in which the supply was made OR the date of filing of the relevant annual return, whichever is earlier.

Let us understand the time limit for issue of credit note with an example.

Example

Super Cars Ltd sells spare parts worth Rs. 6,00,000 to its dealer Ravindra Automobiles on 1st November ‘17.  On 2nd November ’17, Ravindra Automobiles returned spare parts worth Rs 1,00,000, being damaged goods. Super Cars Ltd wants to raise a credit note for the goods returned.

Let us ascertain the last date by when Super Cars Ltd must issue the credit note using 2 scenarios-

Scenario 1- They file annual return of the Financial Year 17-18 on 1st December ‘18

Scenario 2- They file annual return of the Financial Year 17-18 on 31st May ‘18.

| Scenario | Date of original supply | Annual return filing date | Condition for determining last date to issue credit note | Last date for issuing credit note |

|---|---|---|---|---|

| Scenario 1 | 1st November 2017 | 1st December ‘18 | 30th September following the end of the financial year in which the supply was made or the date of filing annual return, whichever is earlier | 30th September ‘18 |

| Scenario 2 | 31st May ‘18 | 31st May ‘18 |

What details should debit notes, supplementary invoices and credit notes include?

Debit notes, supplementary invoices and credit notes must include the following details:

| Debit note/Supplementary Invoice/Credit Note |

|---|

| Nature of the document must be indicated prominently, such as ‘revised invoice’ or ‘supplementary invoice’ |

| Name, address, and GSTIN of the supplier |

| A consecutive serial number containing only alphabets and/or numerals, unique for a financial year |

| Date of issue of the document |

| If recipient is registered- Name, address and GSTIN/Unique ID number of the recipient |

| If recipient is unregistered- Name, address of recipient and address of delivery, with state name and code |

| Serial number and date of the original tax invoice or bill of supply |

| Taxable value of the goods or services, rate of tax and the amount of tax credited or debited to the recipient |

| Signature or digital signature of the supplier or his authorized representative |

How is the Value of Goods & Services Determined under GST?

| Tax | Value of goods/services |

| Excise | Based on transaction value or quantity of goods or MRP |

| VAT | Based on sale value |

| Service Tax | Based on taxable value of service rendered |

Valuation of goods and services

Current tax regime

Let us look at how the value of goods and services is calculated in the current regime, with the help of an example:

Super Cars Ltd, a car manufacturer, sells spare parts to Ravindra Automobiles, their dealers for Rs 6,000. The MRP of the spare parts is Rs 10,000. The invoice that is issued to Ravindra Automobiles is illustrated below:

Under GST Regime

We have used the same example as above to illustrate the method of valuation of goods and services in the GST regime:

*Assuming GST of 18% on automobile spare parts

In the GST regime, the value of goods &/or services supplied is the transaction value, i.e. the price paid/payable, which is Rs 6,000 in the example.

Additional Charges and Expenses – in the GST Regime

How are additional charges and expenses such as discount, packing charges treated in the GST regime? Should they be included or excluded from the transaction value?

Let us consider this illustration.

Super Cars Ltd sells a car worth Rs 4,00,000 to Ravindra Automobiles.

- They incur packing charges of Rs 5,000 on the car

- They provide a discount of 1% on the price, as part of Diwali scheme

- Super Cars Ltd agree to provide a further discount of 0.5% if Ravindra Automobiles makes payment by 31st of the month via net banking. Ravindra Automobiles makes the payment by 31st of the month using net banking.

The invoice issued to Ravindra Automobiles, under GST, will look like this:

*Assuming GST of 18% on car

In the invoice,

- Packing charge of Rs 5,000 is included in the transaction value.

Packing charges or any incidental expenses charged before or at the time of supply of goods or services must be included in the transaction value.

- Discount of 1% is deducted from the transaction value.

Discount given before or at the time of supply, and which is recorded in the invoice, can be deducted from the transaction value.

- Discount of 0.5% is not deducted in the invoice. As discount of 0.5% is given after the supply, it will not be shown in the invoice. However, since the discount was known at the time of supply, and can be linked to this specific invoice, the discount amount can be reduced from the transaction value. For this, Super Cars Ltd will issue a credit note to Ravindra Automobiles for Rs 2,360 (0.5% of Rs 4,00,000 = Rs 2,000+ GST@ 18% on Rs 2,000 = Rs 360), and the same must be linked to the relevant tax invoice.

Discount given after supply but agreed upon before or at the time of supply and can be specifically linked to relevant invoices, can be deducted from the transaction value.

What are the exceptions to this rule?

Answer: Discount given after supply, and not known at the time of supply.

Let us understand this with an illustration.

Super Cars Ltd sells a car to Ravindra Automobiles for Rs 4,00,000. As per the standing agreement, a credit period of 30 days is allowed for payment. However, due to a severe cash crunch, Super Cars Ltd requests Ravindra Automobiles to make the payment within 2 days, promising a discount of 2% on doing so. Ravindra Automobiles makes the payment within 2 days.

In this scenario, since the discount was not known at the time of supply, it cannot be claimed as a deduction from the transaction value for GST calculation.

A summary of the effect of discount on transaction value is given below-

| Type of discount | Effect on transaction value |

| If the discount is given before or at the time of supply, and is recorded in the invoice | Can be claimed as deduction from transaction value |

| If the discount is given after supply, but agreed upon before or at the time of supply, and can be specifically linked to relevant invoices | Can be claimed as deduction from transaction value |

| If the discount is given after supply, and not known at the time of supply | Cannot be claimed as deduction from transaction value |

Effect of various charges/expenses of supply on transaction value is shown below-

| Charges/expenses related to supply | Effect on transaction value |

| Incidental expenses such as commission and packing | Included in transaction value |

| Interest/late fee/penalty charged by supplier for delayed payment | Included in transaction value |

| Subsidies excluding those provided by the Central and State governments | Included in transaction value |

| Any tax other than GST | Included in transaction value |

| Any amount payable by supplier, but incurred by receiver | Included in transaction value |

It is expected that GST (Goods and Services Tax) will bring about marked changes in the tax scenario in the country. The various aspects of product pricing, valuation of goods and services, and others will experience significant transformation as the tax system is simplified.

Moving to GST Era: For Registered Manufacturers

The first and foremost task for you, as a business registered under the current law, is transiting to GST (Goods and Services Tax). While it is important to know the fundamentals of GST, it is also very critical for you to understand GSTÂ transition provisions available, and take necessary actions to ensure a smooth transition to GST and leverage on transition benefits.

You will need to review your accounting and reporting procedures, procurement, logistic decisions, and so on in advance to avail the appropriate GST input tax credit.

For better and ease of understanding, we have categorised GST transition provisions for each of the below business types:

- GST for Manufacturer

- GST for Trader

- GST for Service Provider

GST for Manufacturers

Some questions you may have:

- What will happen to the balance input tax credit available on the last day, before GST to be implemented?

- What will happen to the input tax credit on capital goods which is yet be availed?

Today, the manufacturing and sales activity is governed by a separate indirect tax system. Manufacturing activity is covered by Central Excise and Sales is covered under State VAT/CST. Typically, a manufacturer should be registered under Excise as well as State VAT/CST.

As a manufacturer, you need a thorough understanding about the related provisions, and very importantly, you need to know the answer to “what should I do today for tomorrow’s GST readiness?â€

Scenario 1: Availed CENVAT and Input VAT Credit

The balance CENVAT and input VAT credit available on the last day, prior to date on which GST is implemented, can be carried forward as Input credit.

What does this mean?

- The closing balance of CENVAT and input VAT credit should be reflected in the last return filed by you

- The credit as reflecting in the return should be allowed as CENVAT and input VAT under current law, and

- It should also be allowed as input tax credit under GST

Today, a manufacturer other than the Small Scale Industries (SSI- whose turnover does not exceed Rs 4 crores) should file their monthly returns in Form ER-1, and  SSI quarterly returns in Form ER-3. They also need to file monthly or quarterly VAT return forms, as prescribed by their respective states. The amount of CENVAT carried forward in Form ER-1 or Form ER-3 as on the last day i.e., the day before GST is implemented will be allowed to be carried forward as CGST (Central GST) input tax credit. The input VAT credit in VAT return forms will be carried forward as SGST (State GST) input tax credit.

Let’s understand this with an example –

Super Cars Pvt Ltd, a car manufacturer located in Karnataka is registered under Excise and Karnataka VAT. As on 31st March, 2017, the Form ER-1 and VAT Form 100 (monthly return form for Karnataka) of Super Cars Pvt Ltd is as given below:

| FORM E.R.-1 | ||||||||||

| RETURN OF EXCISEABLE GOODS AND AVAILMENT OF CENVAT CREDIT FOR THE MONTH OF MARCH AND YEAR 2017 | ||||||||||

|

DETAILS OF CREDIT

|

CENVAT

|

AED_TTA

|

NCCD

|

ADE_LVD_CL_85

|

ADC_LVD_CT_75

|

EDU_CESS

|

SEC_EDU_CESS

|

SERVICE_TAX

|

EDU_CESSST

|

SEC_EDU_CESS_ST

|

| Closing Balance | 25,000.00 | 0.00 | 0.00 | 0.00 | 0.00 | 0.00 | 0.00 | 0.00 | 0.00 | 0.00 |

Â

| Form VAT 100 (See rule 138) | |

| RETURN | |

| Tax period (month/quarter) | March, 2017 |

| Credit/excess payment carried forward | 5,000.00 |

As per Form ER-1 and VAT Form 100 of March 2017, Super Cars Pvt Ltd has a closing CENVAT balance of Rs 25,000 and input VAT credit of Rs 5,000. Can Super Cars Pvt Ltd. carry forward the CENVAT and input VAT credit?

Yes, the closing CENVAT balance of Rs 25,000 and Input VAT of Rs 5,000 are fully eligible for Super Cars Pvt Ltd to carry forward. This is because Super Cars Pvt Ltd. satisfies all the 3 conditions explained below:

- The CENVAT of Rs 25,000 and input VAT of Rs 5,000 are carried forwarded in the return.

- Under the current statute, CENVAT and Input VAT are allowed as Input Tax Credit.

- In GST, the same is allowed as Input Tax Credit.

Now, for Super Cars Pvt Ltd, CENVAT will be a CGST credit, and Input VAT will be carried forwarded as SGST credit. This can be utilized to set-off the liabilities in the order as prescribed.

Scenario 2: Unavailed CENVAT credit and Input VAT on capital goods

Currently, under Central Excise, CENVAT credit should be availed to the extent of 50% in the current year, and the remaining in the subsequent year. Similarly, VAT paid on purchase of capital goods will not be fully available as Input VAT immediately. Depending upon the state VAT laws and the type of capital goods purchased, the Input VAT can be availed,

- In instalments spread over different financial years

- As credit after commencement of commercial production

- At reduction value, and so on.

Due to this prevailing restriction for availing CENVAT credit on capital goods, there could be some unavailed CENVAT and Input VAT on the date of transitioning to GST.

Let us discuss with an example to understand better

Super Cars Pvt Ltd purchased machinery on 1st February, 2017. The details of the transaction are shown below:

| Particulars | Amount (Rs) |

| Machinery | 1,00,000 |

| Excise Duty @12.5% | 12,500 |

| VAT @14.5% | 16,313 |

| Total | 1,28,813 |

As per the current CENVAT provisions, Super Cars Pvt Ltd is allowed to avail CENVAT up to 50% in the current year, and the remaining during the subsequent years. Also, according to the VAT provisions of Karnataka, input VAT credit can be availed only after commencement of commercial production. Let’s assume that commercial production was to begin in the month of June’17.

Considering the scenario – Super Cars Pvt Ltd availed

- 50% CENVAT i.e. Rs 6,250 in the current year (2016-17).

- Remaining CENVAT of Rs 6,250 in subsequent year (2017-18).

- Input VAT credit after commencement of commercial production, eligible in 2017-18.

Will Super Cars Pvt Ltd be allowed to carry forward the unavailed CENVAT of Rs 6,250 and input VAT credit of Rs 16,313 on transition to GST?

Yes, Super Cars Pvt Ltd is allowed to carry forward the unavailed CENVAT credit on capital goods, provided these conditions are satisfied:

- Under the current statute, CENVAT and input VAT are allowed as input tax credit.

- It is admissible as input tax credit in GST.

Super Cars Pvt Ltd satisfies all the conditions, and they are eligible to carry forward the CENVAT and input VAT credit.

GST Composition Levy Explained

The current state indirect tax regime has provided a simpler compliance for small dealers known as the Composition Scheme. Under this scheme you,

- Pay taxes only at a certain percentage of turnover

- File periodic returns only (usually on a quarterly basis)

- Have an option of not having to maintain detailed records or follow tax invoicing rules

- Are not allowed to take Input Tax Credit (ITC)

- Are not allowed to collect tax on sales

Thus for smaller businesses, it is simpler to calculate tax liability. This saves time and energy involved in maintaining detailed records.

Let us understand how the composition scheme is different with the following example:

Composition Levy in the GST Regime

Similarly, the same benefit is provided under the GST regime. Small dealers and businesses could opt for the composition scheme known as Composition Levy. Under this scheme, a Composite Tax Payer pays tax only at a certain percentage of his turnover.

Threshold Limit

- NE Including Sikkim – Aggregate turnover of the person having same PAN of above Rs 10 lakhs during the financial year but does not exceed Rs 50 lakhs.

- Rest of India – Aggregate turnover of the person having same PAN of above Rs 20 lakhs during the financial year but does not exceed Rs 50 lakhs.

Rate of Levy

- Rate of levy is yet be notified

- Rate of levy will not be less than 1%

Conditions for a Composite Tax Payer

Apart from the threshold limit, the following conditions are applicable for a composite tax payer:

- No Interstate supplies – A composite tax payer should not engage in interstate supply of goods and / or services and imports.

- Payment of composition tax – If the composite tax payer is in the trade of supplying goods and services, then composition levy will be applicable for both supply of goods and supply of services.

- Does not have to collect tax – The composite tax payer does not have to collect tax on all his outward supply of goods and / or services.

- Applicable for all business verticals under the same PAN – Composition levy will be applicable for all business verticals operating within state or interstate under the same pan.

What does this mean?

An individual with different business verticals, like:- Mobiles & Accessories

- Stationery

- Franchisee

In the above scenario, the composition scheme will be applicable for all three business verticals. The dealer cannot opt for any one business vertical to fall under the composition scheme.  For example, if the business vertical’s place of business is in Karnataka & Kerala for a single PAN, each of the business vertical in that particular state should have only ‘Intra-State(within state)’ supplies.

- Cannot claim Input Tax Credit – The composite tax payer is not eligible to claim input tax credit on all his inward supply of goods and / or services.

What does this mean?

If a dealer chooses to be a composite tax payer, he cannot claim input tax credit even if he makes taxable purchases from a regular taxable dealer. Ideally, the taxable amount would be added to the composite tax payer’s cost.

Return Forms for a Composite Tax Payer

A composite tax payer is required to file quarterly return and annual return. Types of returns and details to be furnished are explained below:

| Return Type | Frequency | Due date | Details to be furnished |

| Form GSTR-4A | Quarterly | — | Auto-populated details of inward supplies made available to the recipient registered under composition scheme on the basis of FORM GSTR-1 furnished by the supplier. |

| Form GSTR-4 | Quarterly | 18th of succeeding month | All outward supplies of goods and services including auto-populated details from Form GSTR-4A and tax payable details. Details of any additions, modifications, or deletions in Form GSTR-4A should also be submitted in Form GSTR-4. |

| Form GSTR-9A | Annual | 31st December of next fiscal | Consolidated details of quarterly returns filed along with tax payment details. |

In the current composition scheme, a composite dealer has to declare only the aggregate turnover of sales. He is not required to declare invoice wise details. In GST, the composite tax payer will file his returns with the invoice wise details of inward supplies which is auto-populated based on Form GSTR-1 filed by his supplier along with the aggregate turnover of outward supplies.

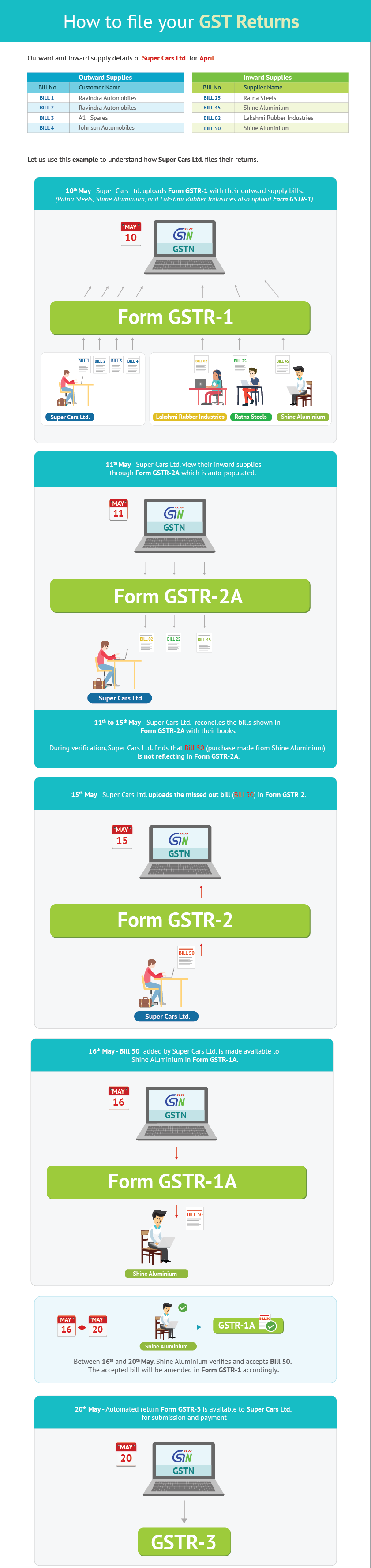

How to File Your GST Returns

Every registered taxable person has to furnish outward supply details in Form GSTR-1 by the 10th of the subsequent month. On the 11th, the visibility of inward supplies is made available to the recipient in the auto-populated GSTR-2A. The period from 11thto 15th will allow for any corrections (additions, modifications and deletion) in Form GSTR-2A and submission in Form GSTR-2 by 15th of the subsequent month.The corrections (addition, modification and deletion) by the recipient in Form GSTR-2 will be made available to supplier in Form GSTR-1A. The supplier has to accept or reject the adjustments made by the recipient. The Form GSTR-1 will be amended according to the extent of correction accepted by supplier.

On 20th, the auto-populated return GSTR-3 will be available for submission along with the payment. After the due date of filing the monthly return Form GSTR-3, the inward supplies will be matched with the outward supplies furnished by supplier, and then the final acceptance of input tax credit will be communicated in Form GST ITC-1.

Also, the mismatch input tax credit on account of excess claims or duplication claims will be communicated in Form GST ITC-1.Discrepancies not ratified will be added as output tax liability along with interest. However, within the prescribed time, if it is ratified, the recipient will be eligible to reduce this output tax liability.

Let us understand this with an example.

What are the Types of Returns Under GST?

Consider what happens today. A manufacturer who is compliant under Central Excise, Service Tax, and VAT has to file returns as specified by each of the states. The manufacturer has to deal with returns, annexures, and registers for Excise, Service tax and VAT with monthly, quarterly, half-yearly and yearly periodicity.

With GST in place, it does not matter whether you are a trader, manufacturer, reseller or a service provider, you only need to file GST returns.

Wow! This sounds good. Let us understand different types of return forms in GST.

Under GST, there are 19 forms for filing of returns by tax payers. All these forms are required to be e-filed. The details of each form are listed below along with details of applicability and periodicity.

Regular Dealer

| Form Type | Frequency | Due Date | Details to be Furnished |

| Form GSTR-1 | Monthly | 10th of succeeding month | Furnish details of outward supplies of taxable goods and/or services affected |

| Form GSTR-2A | Monthly | On 11th of succeeding Month | Auto-populated details of inward supplies made available to the recipient on the basis of Form GSTR-1 furnished by the supplier |

| Form GSTR-2 | Monthly | 15th of succeeding month | Details of inward supplies of taxable goods and/or services claiming input tax credit. Addition (Claims)Â or modification in Form GSTR-2A should be submitted in Form GSTR-2. |

| Form GSTR-1A | Monthly | 20th of succeeding month | Details of outward supplies as added, corrected or deleted by the recipient in Form GSTR-2 will be made available to supplier |

| Form GSTR-3 | Monthly | 20th of succeeding month | Monthly return on the basis of finalization of details of outward supplies and inward supplies along with the payment of amount of tax |

| Form GST ITC-1 | Monthly | — | Communication of acceptance, discrepancy or duplication of input tax credit claim |

| Form GSTR-3A | — | — | Notice to a registered taxable person who fails to furnish return under section 27 and section 31 |

| Form GSTR-9 | Annually | 31st Dec of next fiscal | Annual Return – furnish the details of ITC availed and GST paid which includes local, interstate and import/exports. |

Composite Tax Payer

| Return Type | Frequency | Due Date | Details to be Furnished |

| Form GSTR-4A | Quarterly | — | Details of inward supplies made available to the recipient registered under composition scheme on the basis of Form GSTR-1 furnished by the supplier |

| Form GSTR-4 | Quarterly | 18th of succeeding month | Furnish all outward supply of goods and services. This includes auto-populated details from Form GSTR-4A, tax payable and payment of tax. |

| Form GSTR-9A | Annual | 31st Dec of next fiscal | Furnish the consolidated details of quarterly returns filed along with tax payment details. |

Foreign Non-Resident Taxpayer

| Return Type | Frequency | Due Date | Details to be Furnished |

| Form GSTR-5 | Monthly | 20th of succeeding month or within 7 days after the expiry of registration | Furnish details of imports, outward supplies, ITC availed, tax paid, and closing stock |

Input Service Distributor

| Return Type | Frequency | Due Date | Details to be Furnished |

| Form GSTR-6A | Monthly | 0n 11th of succeeding month | Details of inward supplies made available to the ISD recipient on the basis of Form GSTR-1 furnished by the supplier |

| Form GSTR-6 | Monthly | 13th of succeeding month | Furnish the details of input credit distributed |

Tax Deductor

| Return Type | Frequency | Due Date | Details to be Furnished |

| Form GSTR-7 | Monthly | 10th of succeeding month | Furnish the details of TDS deducted |

| Form GSTR-7A | Monthly | TDS certificate to be made available for download | TDS Certificate – capture details of value on which TDS is deducted and deposit on TDS deducted into appropriate Govt. |

E-commerce

| Return Type | Frequency | Due Date | Details to be furnished |

| Form GSTR-8 | Monthly | 10th of succeeding month | Details of supplies effected through e-commerce operator and the amount of tax collected on supplies |

Aggregate Turnover Exceeds 1 crore

| Return Type | Frequency | Due Date | Details to be furnished |

| Form GSTR-9B | Annually | Annual, 31st Dec of next fiscal | Reconciliation Statement – audited annual accounts and a reconciliation statement, duly certified. |

Final return

For taxable person whose registration has been surrendered or cancelled

| Return Type | Frequency | Due Date | Details to be furnished |

| Form GSTR-10 | Monthly | Within 3 months of cancellation of registration | Furnish details of inputs and capital goods held, tax paid and payable. |

Government Departments and United Nation Bodies

| Return Type | Frequency | Due Date | Details to be furnished |

| Form GSTR-11 | Monthly | 28th of succeeding month | Details of inward supplies to be furnished by a person having UIN |

How to Amend, Cancel, or Revoke GST Registration

Let us now understand how to:

- Amend your registration details

- Apply for cancellation of registration

- Revoke your registration if it is cancelled

Amending Your Registration Details

- Any change in details furnished at the time of registration must be submitted within 15 days from the date of such changes in Form GST REG-11.

- Specific changes in Form GST REG-11 relating to the name of the business, partner details, managing committee, and so on, require approval from an officer. After verification, an approval order by the officer is sent in Form GST REG-12 to amend the details.

- Changes in business details that result in change of PAN number of the registered tax payer, require a fresh registration in Form GST REG-01.

Applying for Cancellation of Registration

- A registered taxable person seeking cancellation of registration, should submit Form GST REG-14 along with details of closing stock and other relevant documents.

- Within 7 days, a notice in Form GST REG-15 is issued to the taxable person to show cause with reason for such cancellation.

- After verification and approval by an officer, cancellation order in  Form GST REG-16 is issued within 30 days from the date of receipt of Form GST REG-15 or date of show cause.

AÂ taxable person who has voluntarily registered is allowed to apply for cancellation only after completion of 1 year of registration. An officer determines the effective date of cancellation after directing the taxable person to clear any tax arrears and penalty, if any.

Revoking a Cancelled Registration

- In case the registration is cancelled by an officer, a taxable person can apply for revocation by submitting Form GST REG-17 within 30 days from date of cancellation order.

- If the officer requires additional details or clarification, Form GST REG-3 is issued within 3 working days.

- The taxable person then needs to respond by providing requisite details in Form GST REG-4 (within 7 working days).

- If the officer is satisfied, the cancellation is revoked by issuing an order in Form GST REG-18 within 30 days from date of such application.

- If the officer is not satisfied, the revocation application is rejected in Form GST REG-5. Prior to this rejection, the taxable person will be issued a show cause notice in Form GST REG-19 and hearing.