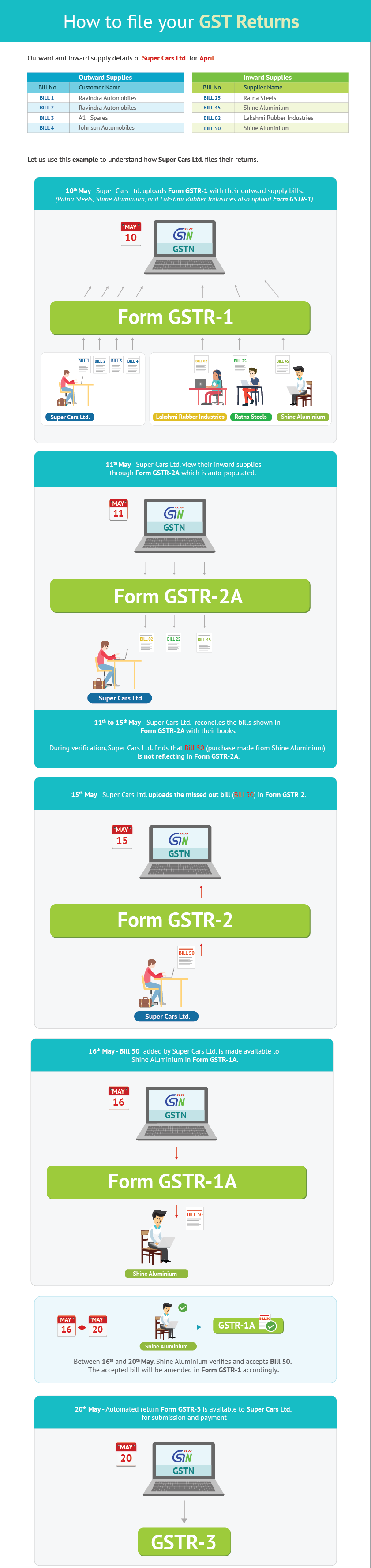

The first and foremost task for you, as a business registered under the current law, is transiting to GST (Goods and Services Tax). While it is important to know the fundamentals of GST, it is also very critical for you to understand GSTÂ transition provisions available, and take necessary actions to ensure a smooth transition to GST and leverage on transition benefits.

You will need to review your accounting and reporting procedures, procurement, logistic decisions, and so on in advance to avail the appropriate GST input tax credit.

For better and ease of understanding, we have categorised GST transition provisions for each of the below business types:

- GST for Manufacturer

- GST for Trader

- GST for Service Provider

GST for Manufacturers

Some questions you may have:

- What will happen to the balance input tax credit available on the last day, before GST to be implemented?

- What will happen to the input tax credit on capital goods which is yet be availed?

Today, the manufacturing and sales activity is governed by a separate indirect tax system. Manufacturing activity is covered by Central Excise and Sales is covered under State VAT/CST. Typically, a manufacturer should be registered under Excise as well as State VAT/CST.

As a manufacturer, you need a thorough understanding about the related provisions, and very importantly, you need to know the answer to “what should I do today for tomorrow’s GST readiness?â€

Scenario 1: Availed CENVAT and Input VAT Credit

The balance CENVAT and input VAT credit available on the last day, prior to date on which GST is implemented, can be carried forward as Input credit.

What does this mean?

- The closing balance of CENVAT and input VAT credit should be reflected in the last return filed by you

- The credit as reflecting in the return should be allowed as CENVAT and input VAT under current law, and

- It should also be allowed as input tax credit under GST

Today, a manufacturer other than the Small Scale Industries (SSI- whose turnover does not exceed Rs 4 crores) should file their monthly returns in Form ER-1, and  SSI quarterly returns in Form ER-3. They also need to file monthly or quarterly VAT return forms, as prescribed by their respective states. The amount of CENVAT carried forward in Form ER-1 or Form ER-3 as on the last day i.e., the day before GST is implemented will be allowed to be carried forward as CGST (Central GST) input tax credit. The input VAT credit in VAT return forms will be carried forward as SGST (State GST) input tax credit.

Let’s understand this with an example –

Super Cars Pvt Ltd, a car manufacturer located in Karnataka is registered under Excise and Karnataka VAT. As on 31st March, 2017, the Form ER-1 and VAT Form 100 (monthly return form for Karnataka) of Super Cars Pvt Ltd is as given below:

| FORM E.R.-1 | ||||||||||

| RETURN OF EXCISEABLE GOODS AND AVAILMENT OF CENVAT CREDIT FOR THE MONTH OF MARCH AND YEAR 2017 | ||||||||||

|

DETAILS OF CREDIT

|

CENVAT

|

AED_TTA

|

NCCD

|

ADE_LVD_CL_85

|

ADC_LVD_CT_75

|

EDU_CESS

|

SEC_EDU_CESS

|

SERVICE_TAX

|

EDU_CESSST

|

SEC_EDU_CESS_ST

|

| Closing Balance | 25,000.00 | 0.00 | 0.00 | 0.00 | 0.00 | 0.00 | 0.00 | 0.00 | 0.00 | 0.00 |

Â

| Form VAT 100 (See rule 138) | |

| RETURN | |

| Tax period (month/quarter) | March, 2017 |

| Credit/excess payment carried forward | 5,000.00 |

As per Form ER-1 and VAT Form 100 of March 2017, Super Cars Pvt Ltd has a closing CENVAT balance of Rs 25,000 and input VAT credit of Rs 5,000. Can Super Cars Pvt Ltd. carry forward the CENVAT and input VAT credit?

Yes, the closing CENVAT balance of Rs 25,000 and Input VAT of Rs 5,000 are fully eligible for Super Cars Pvt Ltd to carry forward. This is because Super Cars Pvt Ltd. satisfies all the 3 conditions explained below:

- The CENVAT of Rs 25,000 and input VAT of Rs 5,000 are carried forwarded in the return.

- Under the current statute, CENVAT and Input VAT are allowed as Input Tax Credit.

- In GST, the same is allowed as Input Tax Credit.

Now, for Super Cars Pvt Ltd, CENVAT will be a CGST credit, and Input VAT will be carried forwarded as SGST credit. This can be utilized to set-off the liabilities in the order as prescribed.

Scenario 2: Unavailed CENVAT credit and Input VAT on capital goods

Currently, under Central Excise, CENVAT credit should be availed to the extent of 50% in the current year, and the remaining in the subsequent year. Similarly, VAT paid on purchase of capital goods will not be fully available as Input VAT immediately. Depending upon the state VAT laws and the type of capital goods purchased, the Input VAT can be availed,

- In instalments spread over different financial years

- As credit after commencement of commercial production

- At reduction value, and so on.

Due to this prevailing restriction for availing CENVAT credit on capital goods, there could be some unavailed CENVAT and Input VAT on the date of transitioning to GST.

Let us discuss with an example to understand better

Super Cars Pvt Ltd purchased machinery on 1st February, 2017. The details of the transaction are shown below:

| Particulars | Amount (Rs) |

| Machinery | 1,00,000 |

| Excise Duty @12.5% | 12,500 |

| VAT @14.5% | 16,313 |

| Total | 1,28,813 |

As per the current CENVAT provisions, Super Cars Pvt Ltd is allowed to avail CENVAT up to 50% in the current year, and the remaining during the subsequent years. Also, according to the VAT provisions of Karnataka, input VAT credit can be availed only after commencement of commercial production. Let’s assume that commercial production was to begin in the month of June’17.

Considering the scenario – Super Cars Pvt Ltd availed

- 50% CENVAT i.e. Rs 6,250 in the current year (2016-17).

- Remaining CENVAT of Rs 6,250 in subsequent year (2017-18).

- Input VAT credit after commencement of commercial production, eligible in 2017-18.

Will Super Cars Pvt Ltd be allowed to carry forward the unavailed CENVAT of Rs 6,250 and input VAT credit of Rs 16,313 on transition to GST?

Yes, Super Cars Pvt Ltd is allowed to carry forward the unavailed CENVAT credit on capital goods, provided these conditions are satisfied:

- Under the current statute, CENVAT and input VAT are allowed as input tax credit.

- It is admissible as input tax credit in GST.

Super Cars Pvt Ltd satisfies all the conditions, and they are eligible to carry forward the CENVAT and input VAT credit.